28 November 2024

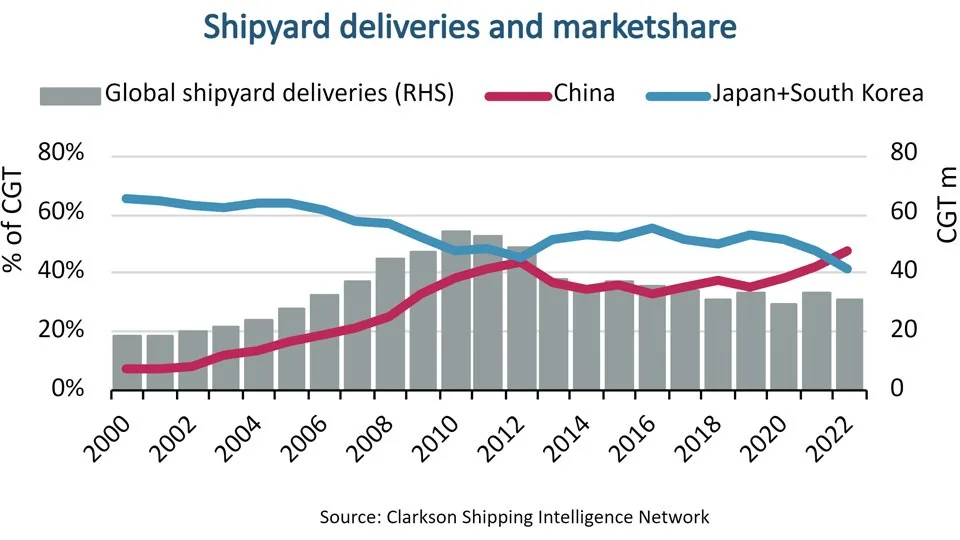

Chinese shipyards hit new record 49% market share in 2022

In 2022, Chinese shipyards reached a market share of 49% and for the first time exceeded the combined market share of Japanese and South Korean shipyards.

Table of Contents

In 2022, Chinese shipyards reached a market share of 49% and for the first time exceeded the combined market share of Japanese and South Korean shipyards.

While global newbuild order volumes fell (20% y-o-y in CGT terms), 2022 was still an active year for the global shipbuilding industry with higher pricing (up 15% on average), more complex ships ordered (e.g. a record 182 LNG orders of $39bn) and alternative fuel investment increasing (a record 61% of tonnage ordered) all supporting a 6% increase in value of orders to $124.3bn.

What is CGT?

Compensated Gross Tonnage (CGT) was introduced by the OECD in 2007 as a unit of measurement that would objectively reflect the relative production capacity in various shipyards and in different regions of the world. The CGT value is calculated for specific types of ships, not for all floating objects.

Ships of similar volume (that is to say, of similar dimensions) will have a very similar Gross Tonnage (GT) value. However, the utilization of the ship’s available volume resulting from the ship’s type may differ significantly. The more complex unit will have a higher CGT value than the less complex unit.

Chinese Shipyards at the Top

Ships delivered to new owners by Chinese shipyards in 2022 totalled 14.6 million Compensated Gross Tonne (CGT). Note that, the global measure of shipyard activity, is 30.8 million CGT delivered. The two other main shipbuilding nations, Japan and South Korea, delivered respectively 4.8 and 7.8 million CGT.

Twenty years ago, Chinese shipyards had a market share of less than 10% but a massive capacity expansion during the 2000s propelled the country to the number one spot already in 2009.

The shipyards in China also dominate the order book for ships to be delivered in the coming years. The global order book currently totals 109.1 million CGT, and 45% of those orders are held by Chinese yards compared to 34% and 10% by South Korean and Japanese yards respectively.

From an owner perspective, China ($18.4bn), Japan ($15.1bn), and Italy ($11bn) contributed 36% of the investment but Greek owners “kept their powder dry” (“only” $8.5 bn).

Vessel types

Chinese shipyards’ success (49%) has been achieved by maintaining a leading position within dry bulk ships and, more recently, establishing themselves as the premier location for building container ships. They also hold a large share of orders for most other ship types but have yet to establish themselves as key players within the gas carrier sector.

LNG carriers are currently the second largest ship sector (record 182 vessels, 36% CGT) within the global order book for ships, and South Korean shipyards remain the market leaders within this sector, holding 79% of the order book.

Currently, Chinese shipyards hold only 15% of the LNG carrier order book, but they could make inroads also into this sector, just like they gradually attracted orders for ultra large container ships.

More than 160 LNG carriers ordered in 2022

The year 2022 saw an ordering spree for LNG carriers, amid spiking demand for LNG driven by the ongoing geopolitical turbulence in Europe.

Ship Nerd

Further Competition

In the short term, yards in other countries are unlikely competitors and China, South Korea, and Japan are likely to maintain their combined nearly 90% market share.

In search of lower costs, countries like Vietnam and the Philippines could become larger competitors in the future; similar to how the center of shipbuilding historically moved from Europe to Japan and onwards to South Korea and China.

European output has stabilized (at 2.5m CGT and 8% of global market share helped by Cruise deliveries). We are projecting that output will start to tick up (by ~6% in 2023), become increasingly dominated by container and LNG (41% of 2023 scheduled deliveries, rising to 58% in 2024), and that South Korean output share will tick upwards.

With only 131 “large” active yards (2009: 320), the estimated shipbuilding capacity is about 40% lower than a decade ago.

Fleet Renewal & Alternative Fuels

At the heart of reducing shipping’s 2.3% (855mt) contribution to global CO2 will be an unprecedented fuelling transition and projected increasing underlying fleet renewal requirements as the decade develops (see Shipping & Shipbuilding Forecast Forum). The entry into force of IMO “short-term measures” (EEXI, CII) is a hugely significant milestone in shipping’s decarbonization pathway (as will the EU’s ETS be in 2024) and is a market “wildcard”.

MEPC 79 – New amendments & IMO GHG Strategy

What are the new amendments and GHG strategy that resulted from the IMO MEPC 79? This is everything you need to know.

Ship Nerd

Across 2022, 61% of tonnage ordered (35% by number) was alternatively fuelled (World Fleet Register). Over half of the tonnage ordered (397 orders, 36.7m GT) was LNG dual fuel, 7.0% was methanol (43 orders, 5.0m GT), 1.1% LPG (17 orders, 0.8m GT) and 1.2% included battery hybrid. 10.8% of orders were ammonia “ready” (90 orders, 7.7m GT), 1.4% of orders were LNG “ready” (31 orders), 0.1% were hydrogen “ready” and 22 orders were methanol “ready”.

Although long-term trends point to increasing fleet renewal, 2023 will have its marketing challenges for yards: macro-economic risk is material and may weigh on investor sentiment, alternative fuel choices remain tricky and newbuild prices and berth availability are a hurdle for some owners. But there are “mitigating” factors for shipping and the product mix is likely to change: the container market will be weaker (although don’t rule out orders, possibly in feeders) but tankers and bulkers have historically low orderbooks (4% and 6% of fleet). Along with currency and inflation (perhaps some easing), yards will need to be as agile as ever.

See Also

The Problems for South Korea Shipbuilding Industry

South Korean shipbuilders had led the industry but are facing growing challenges and recently slipped back into second place for new orders.